[Introduction: The Invisible Thief in Your Villa]

You’ve done the hard work. You’ve calculated your “Freedom Number” with precision. You’ve scouted the perfect low-cost-of-living (LCOL) destination. But as a strategic capitalist, you must face a hard truth: $2,500 today is not the same as $2,500 twenty years from now.

Inflation is the invisible thief that steals the purchasing power of your hard-earned capital while you sleep. If your financial plan is static, it is dying. To truly retire early and stay retired, you need a dynamic strategy that doesn’t just “save” money but “grows” purchasing power. In this comprehensive guide, we will dismantle the myth of the static retirement fund and build an “Inflation-Proof Shield” for your global lifestyle.

Section 1: The Mathematics of Eroding Value

To beat an enemy, you must first understand its power. Inflation is the rate at which the general level of prices for goods and services rises. When inflation hits, every dollar you own buys a smaller percentage of a good or service.

A. The Compounding Trap in Reverse

We often talk about the “Magic of Compounding” for growth, but inflation is compounding in reverse. Even at a modest 3% annual inflation rate, the value of your money halves approximately every 24 years.

The formula for the future cost of your lifestyle is:

FV=PV×(1+r)n

(Where FV is Future Value, PV is Present Value, r is the inflation rate, and n is the number of years.)

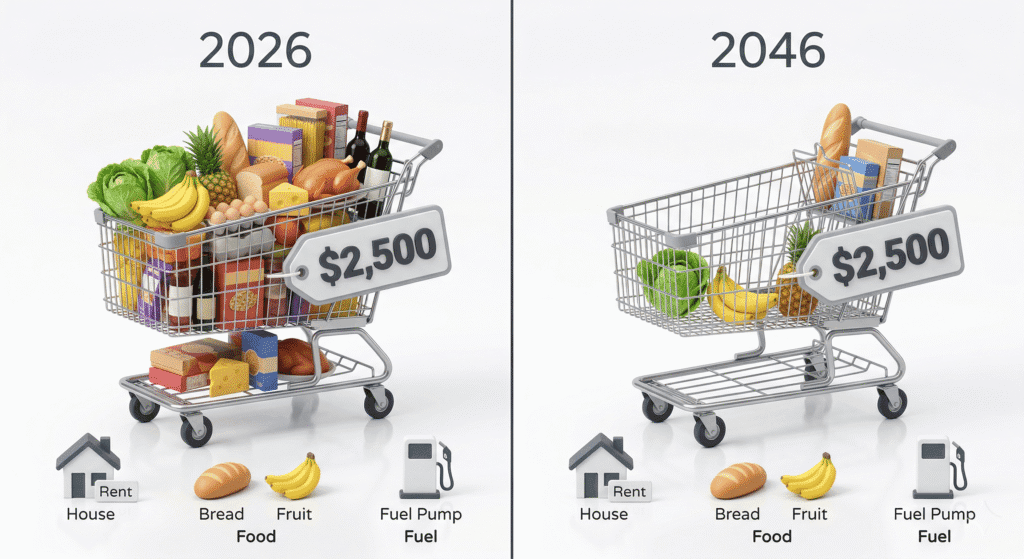

B. The 30-Year Reality Check (Comparison Table)

If you start your geo-arbitrage journey with a $2,500/month budget, here is what you will need to maintain the exact same quality of life over three decades:

| Year | Monthly Budget Needed (3% Inflation) | Annual Total Required | Total Portfolio Needed (4% Rule) |

| 2026 (Now) | $2,500 | $30,000 | $750,000 |

| 2036 (10 yrs) | $3,360 | $40,320 | $1,008,000 |

| 2046 (20 yrs) | $4,515 | $54,180 | $1,354,500 |

| 2056 (30 yrs) | $6,068 | $72,816 | $1,820,400 |

Capitalist’s Note: If you only aim for $750,000 today without an inflation-adjusted investment strategy, you will run out of money by year 15.

💡 Strategist’s Note: While general inflation is a risk, medical costs historically rise at a much faster rate. To protect your fund from these specific spikes, read our guide on [Navigating Healthcare and Taxes in Your Geo-arbitrage Journey].

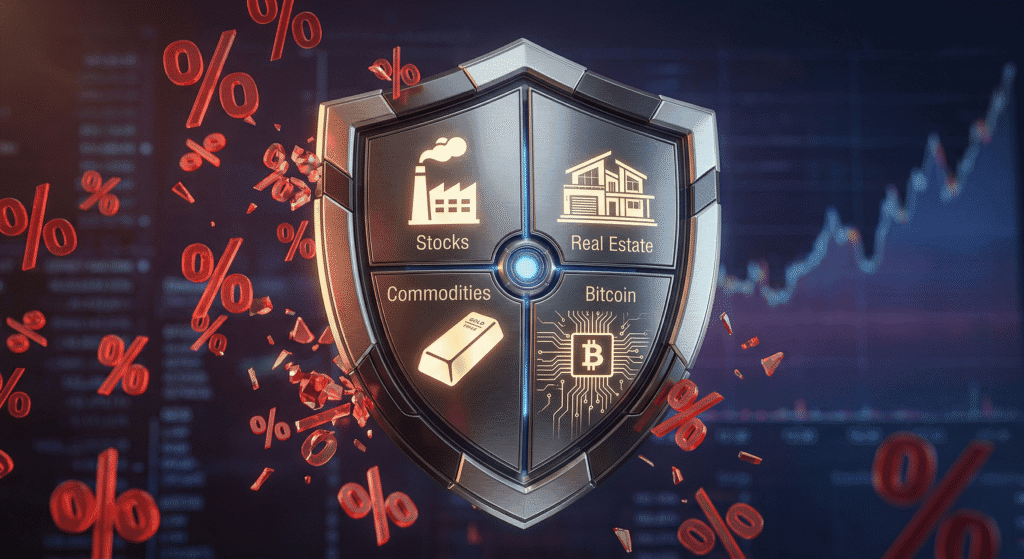

Section 2: Building the Inflation-Proof Portfolio

Cash is your enemy in an inflationary environment. To stay free, your “Freedom Fund” must be composed of assets that have an intrinsic link to the real economy.

1. Equities: The Engine of Growth

Stocks are arguably the best long-term inflation hedge. Why? Because companies have “pricing power.” When the cost of raw materials rises, companies like Apple, Coca-Cola, or Google raise their prices. As an owner (shareholder), you capture that price increase through higher dividends and stock prices.

- Target: Broad-market ETFs (S&P 500 or MSCI World) should form the core (50-70%) of your portfolio.

2. Real Estate: The Hard Asset Hedge

Real estate is a “double-win” against inflation. First, the value of the property tends to rise with inflation. Second, if you rent out a portion of your assets, you can increase the rent every year. For those practicing geo-arbitrage, owning a home in a stable LCOL hub eliminates your biggest inflationary risk: Rent Hikes.

3. Commodities and Bitcoin: The Scarcity Play

In a world of “Infinite Money Printing,” scarcity is king.

- Gold: The traditional “Store of Value” for 5,000 years.

- Bitcoin: Emerging in 2026 as “Digital Gold.” With a hard cap of 21 million coins, it cannot be devalued by any central bank. A small allocation (1-5%) acts as an insurance policy against the collapse of fiat currency purchasing power.

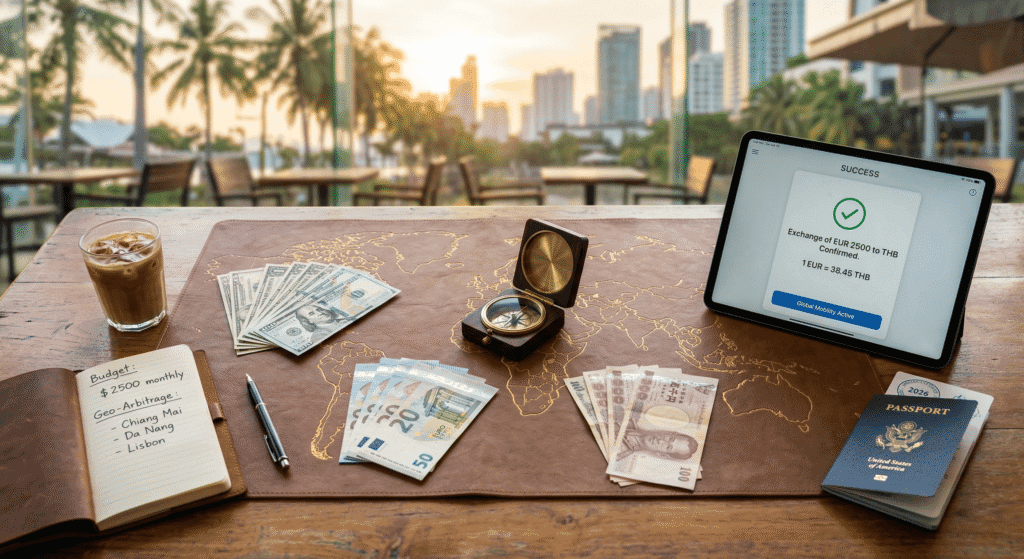

Section 3: Geo-arbitrage—The Ultimate Inflation Cheat Code

One of the most overlooked benefits of the global lifestyle is Currency Arbitrage. You are not just living in another country; you are diversifying your “Cost Base.”

- The USD Dominance: If you earn or hold assets in a strong currency (USD, EUR, CHF) but spend in a developing nation’s currency (THB, VND, MXN), you often find that the exchange rate moves in your favor, neutralizing local inflation.

- Lifestyle Arbitrage: When one region becomes too expensive due to hyperinflation or economic mismanagement, the sovereign individual simply moves to the “next” hub. Your mobility is your greatest financial asset.

Section 4: Advanced Withdrawal Strategies

The famous 4% Rule (The Trinity Study) actually already accounts for inflation. It assumes you withdraw 4% in year one and increase that dollar amount by the inflation rate every year thereafter.

However, for maximum safety in a volatile world, consider the “Guardrail Strategy”:

- The Floor: Never withdraw less than a certain “survival” amount.

- The Ceiling: If the market booms, don’t overspend. Reinvest the excess to cover future inflation spikes.

- The 3.5% Goal: Aim for a 3.5% withdrawal rate instead of 4%. This small 0.5% difference provides a massive buffer against “Sequence of Returns Risk” and unexpected hyperinflation.

Conclusion: Designing for Decades, Not Days

Financial freedom is not a finish line; it is a moving target. By acknowledging the reality of inflation today, you ensure your freedom is permanent. You don’t need a million dollars to be free; you need a system that produces the purchasing power of your desired lifestyle, forever.

Stop fearing the numbers. Start mastering them.

🚀 Is your Freedom Number truly inflation-proof? Don’t leave your future to chance. Use our [Freedom Fund Calculator] to input your adjusted expenses and see if your current target holds up against the next 20 years of inflation.